Home / Blog / Debt

by Janet Doyle

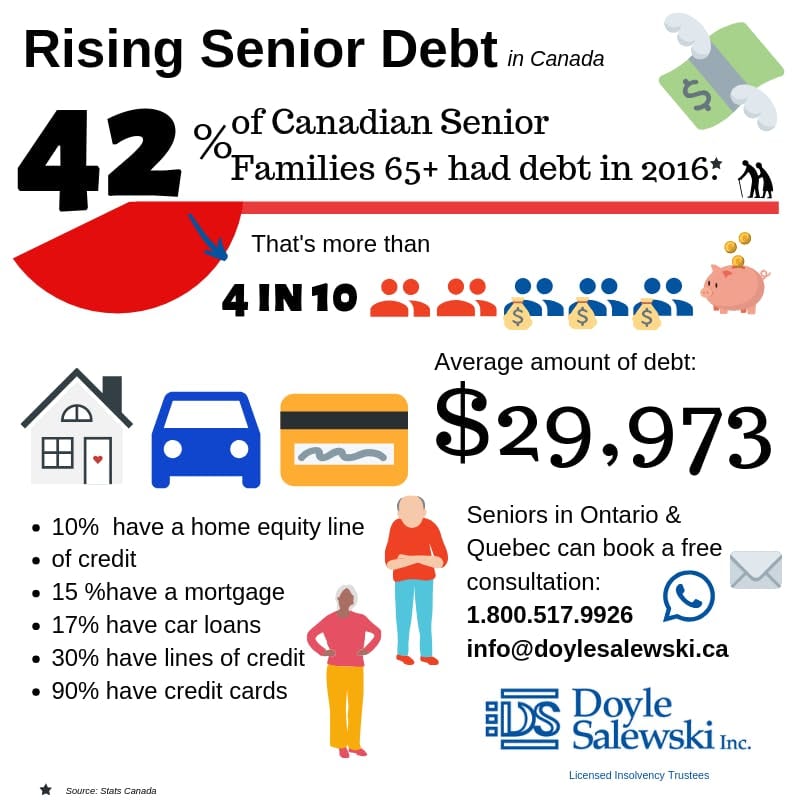

If you’re a senior in debt, you’re not alone. According to a survey, the average Canadian senior carried $29,973 in debt and 30% of Canadians aged 55-70 were still working because they needed to. The Financial Planning Standards Council Foundation found that while 56% of Canadians had debt; 35% of respondents were Canadians 80 or older.

Common debts held by seniors include:

- Installment loan with regular payments for a specific period of time

- credit card debt (32%)

- line of credit (23%)

- mortgage (19%)

- auto-loans (14%).

There are a number of factors that are causing seniors in Canada to become indebted in their golden years. In a recent interview Professor Paul Schwartz at Carleton University told BNN Bloomberg that many seniors in Canada are going into debt to help their adult children. As children struggle with the high costs of student loans and large down payments for homes, parents are swooping in to assist financially and carrying larger debt loads into retirement.

In addition, higher divorce rates have caused financial hardship to families, with more money needed to pay for multiple households, alimony, child support, and legal fees. Couples over the age of 50 have seen increased divorce rates, and dividing incomes can make it challenging to maintain established lifestyles. Seniors have a harder time recovering financially; they have less ability to increase their income, and they may have accumulated several debts. If not prepared for retirement to begin with, the financial burden can become overwhelming for these new single income households.

Of course, with aging comes increased health issues and more associated costs. Prescriptions and long-term care are leading factors causing financial hardship to seniors, who typically see an increase in health issues as they age. At the same time, life expectancy has increased for the average Canadian, stretching retirement income thinner than it has been in previous years. There has been an increased number of Canadians passing away while in debt, forcing their estate into bankruptcy after they are deceased.

With all these factors combined, it’s no surprise that Canadian seniors are racking up debt faster than any other age group. As interest rates and the cost of living continue to rise, more seniors are falling behind on their payments. Delinquency rates for Canadians 65 and older were up by 7.2% year-over-year in the fourth quarter of 2018. With 77% of Canadian seniors reliant on their pension as their primary source of income, many are not able to keep up with rising costs and debt payments, putting their livelihood at risk.

For those receiving Old Age Security and/or Canadian Pension Plan funds, there is a law the protects your benefits from being taken from you if you are sued. If at any point you are taken to court by a creditor, your pension income cannot be used as security on your outstanding debts. These programs are controlled by the government and are not allowed to be re-assigned to anyone other than the Canadian citizen entitled to that pension.

However, there are some special circumstances where this rule does not apply:

- If the funds are held in an account at a bank where you owe money, the bank can seize them to pay outstanding debts at the same institution. Many banks state this in their agreement. If you get behind on a credit card or loan at the institution you do banking with, the bank can take the money out of your savings or chequing account.

- The Canada Revenue Agency can contact your bank or to the offices that administer CPP and OAS benefits and direct the institution to send them any money under a garnishment order. If your CPP is being garnished, the financial institution is required to comply with the CRA unless they receive written confirmation of an assignment in bankruptcy, a consumer proposal, or a notice to file a proposal.

- For those that owe support or maintenance payments for children and/or spouses, 50% of pension income can be seized to pay towards money owning. The government can take the money from your pension to be used to pay outstanding child support debt. In addition, for those behind $3000 or more, your passport can be denied or suspended.

In these 3 situations, your pension income is at risk for being seized. Losing a primary source of income can create further problems as other bills go unpaid; with little to no cashflow, seniors being garnished are at risk for having other legal action or in the case of defaulting on a mortgage, could lose their home.

It’s very difficult to stop a garnishment proceeding on your own once it has been executed. Typically, the only way to deal with it is to pay the debt in full, unless you can come to an agreement with the creditor. Unfortunately, it’s in the creditor’s best interest and legal right to continue with a legal garnishment rather than a voluntary repayment plan, so they are unlikely to accept an informal agreement.

If you meet with Doyle Salewski, we can begin the process to stop a garnishment immediately (with the exception of child support or alimony). As Licensed Insolvency Trustee, we create a formal, government supervised repayment plan based on your personal financial situation that is lawfully binding and offers immediate legal protection to allow you to regain control of your finances. The sooner you act, the sooner we can help, and the less money you lose to the garnishment.

Contact Doyle Salewski if you’re at risk for garnishment, we offer a free personalized consultation with one of our experienced directors that will allow you to evaluate all the options available to you, and help brighten your golden years with a fresh financial start. Email [email protected] or call 1-800-517-9926 to speak to make an appointment today.